")

Cindy Ord/Getty Images Entertainment

Last week, I made the pilgrimage to the Mecca and Medina of High Finance – New York City. The city felt like pre-Covid, back in rhythm, and moving at its usual frenetic pace. The reason for the journey was the opportunity to meet with Mark Penn, CEO of Stagwell Inc. (NASDAQ:NASDAQ:STGW), and Michaela Pewarski, Head of Investor Relations at Stagwell. Zoom calls are fine, but given Mark’s unique career, including a stint as Chief of Strategy at Microsoft (MSFT), it was too compelling not meet in person and get the chance to size this guy up. After a fairly lengthy meeting, I drew the conclusion Mark is bright, bordering on incandescently bright, and just the right leader to be running point for a disruptive marketing company, circa 2022.

Unless you are a dividend investor and happen to own shares in one of the big three of creative advertising, think Omnicom Group Inc. (OMC), The Interpublic Group of Companies, Inc. (IPG), or WPP plc (WPP), chances are you’ve probably never heard of Stagwell Inc. Stagwell Inc. was conceived of and created by Mark Penn and is financially backed (as an equity investor) by Steve Ballmer, the former CEO of Microsoft, back in 2015. The company’s origins and secret sauce is its focus on disruptive digital marketing. The company came public via a buyout of publicly traded MDC Partners Inc., which was completed on August 2, 2021. Given the structure of the merger, there was no splashy IPO, and if there is no splashy and expensive IPO then that means no fat and lucrative underwriting fees for Wall Street. And when there are no juicy fees for Wall Street, sell side coverage and sponsorship is slower, harder, and an uphill ascent. Let’s face it, everyone wants to be covered by Goldman Sachs, JP Morgan, Morgan Stanley, etc. Because of this lack of sell side coverage, chances are you never heard of Stagwell.

Before we dive in, let’s quickly zoom out and take a step back.

For anyone who has ever attended a decent B School or simply closely follows markets and/ or reads a lot then most likely you learned along the way that new entrants, companies that get to start from scratch and with the luxury of a blank canvass, can have a distinct advantage when it comes to recognizing, executing on, and getting an early jump on major emerging growth trends. Often, the large, entrenched, and highly profitable existing businesses are simply too risk averse and overly focused on milking a cash cow business. Why ruffle the feathers of the golden goose when that golden goose continues to lay golden eggs, on a daily basis. Let’s face it, when you are generating mid teens EBITDA margins, on a large revenue base, albeit only growing organic revenue low single digits, and spitting off large quantities of free cash flow, it is harder for an organization operate dynamically.

The classic B school case is Eastman Kodak (KODK). Eastman Kodak was once a technology pioneer that built a fantastic brand, product, and highly profitable business that generated oodles of cash. Lo and behold, when you have a great business, operating in what reasonable people might consider in an oligopoly market structure, it is easy to rest well at night thinking the walls of the city are well guarded, strongly fortified, and have redundant levels of defense. That said, in business, the barbarians are almost always just outside the gate, whether or not you chose to see them is another question and a matter of vantage point. Then again, and just to be clear, I’m not suggest the Big 3 are at risk of being leap frogged per se, like Eastman Kodak was, I’m simply pointing out that disruption occurs all the time and even in oligopolies.

Who Is Stagwell?

To understand Stagwell, let’s quickly discuss MDC Partners. At a very high level, MDC Partners was a boutique company that controlled a number of excellent creative brands, including 72andSunny, Anomaly, Forsman & Bodenfors and Doner. The company punched well above its weight when it came to creative. However, the business was very poorly managed, and the prior management team were bad stewards of shareholders’ capital, in my opinion. Notably, there were accounting issues related to the deferred compensation / earn-outs from acquisitions. Ultimately, though, when you are publicly traded, this is a business and you are accountable to Wall Street, so you have to be consistent and deliver results. So, for the old MDC, on balance, owning strong creative brands was marred by the sins of prior management team. As a result of this mis-management, Stagwell made the leap and moved from a minority equity investor (they initially invested $100 million in the equity) to the 100% controlling buyer of the business, under Mark’s leadership. Mark said the first year involved a lot of clean up work and the installation of basic blocking and tackling, in other words, running this like a real publicly traded business.

Fast forward to today, and you have a company that has assembled a strong collection of brands and has fused creative, technology, digital, and media, among other nooks and crannies of marketing, under one big umbrella. This collective combination of brands and assets enables Stagwell to provide integrated marketing solutions to some of the world’s best businesses and largest buyers of marketing services.

As more CMO (Chief Marketing Officers) are seeking a streamlined, and integrated approach, as managing six to nine different agencies relationships is exhausting and potentially less productive, and let’s not forget there are only so many hours in a day, regardless of your station in life. With Stagwell’s full suite of offerings, they are winning more business with The Who’s Who of Marketing. In fact, Mark said Stagwell built out a strong organization that can deliver a soup to nuts and integrated solution, just like the Big 3.

This approach is working. See exhibit A and exhibit B from Stagwell’s Q2 FY 2022 conference call.

Exhibit A

We’re growing our share of wallet with our largest clients. The average client size among the top 25 has grown from about $4.5 million to about $6 million, a 30% increase.

Exhibit B

I will now discuss the operating results of each of these segments. Beginning with Integrated Agencies, our largest segment, organic net revenue grew by $27 million and $79 million or 9% and 15% in Q2 and for the 6 months, respectively, driven by strength in digital, integrated pitches and larger contract wins. The media network increased its organic net revenue by $36 million and $68 million or 28% and 27% in Q2 and for the 6 months, respectively, driven by demand for our digital services, several $10 million contract wins and growth in our travel-related business. Organic net revenue in the Communications segment increased by $15 million and $30 million or 28% and 30% in Q2 and for the 6 months, respectively, driven by the ramp-up in our Advocacy business in the midterm election year.

Other fast growing and leading brands under the Stagwell umbrella of companies are Code and Theory, GALE, YML, and Advocacy (consisting of Targeted Victory and Allison & Partners SKDK).

Stagwell’s September 2022 Investor Presentation

As I don’t want to risk losing the readership, getting too deep into the weeds, for readers that are intellectually curious, I would encourage you to watch a number of ten to fifteen minute videos presented by the founders or brand presidents of Stagwell’s leading banners (see here – from Stagwell’s November 2021 Investor Day).

The Market Opportunity

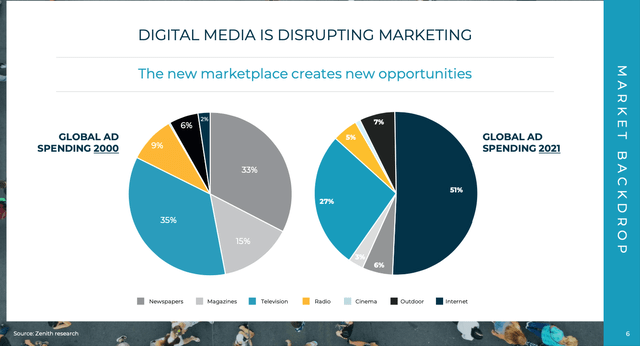

When I spoke with Mark, he framed it this way. Back in 2000, television captured 35% of global ad spending dollars, newspapers 33%, and magazines 15%, with radio, cinema, and outdoor making up the rest of the pie. In 2021, newspaper and magazine combined captured only 9%, television 27%, and internet (digital) accounted for 51%.

Stagwell’s September 2022 Investor Presentation

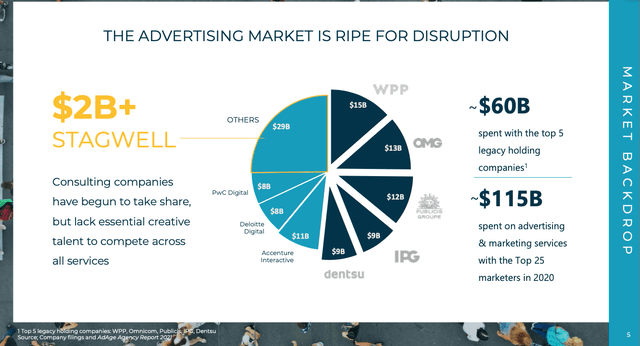

In terms of the total addressable market, in 2020, and according to Zenith Research, Brands spent roughly $115 billion with the Top 25 marketing services companies. The big three, referenced earlier, Omnicom, IPG, and WPP, as well as Publicis Group and dentsu captured $60 billion of that pie. The consulting firms, including Accenture Interactive (ACN), PwC Digital, and Deloitte Digital collectively grabbed $27 billion of the pie, and the remaining $29 billion was split between everyone else. Stagwell is one of those scrappy emerging and fast growing challenger companies that is capturing north of $2 billion of annual revenues.

Although it is a little tricky to precise pin down, and there is some nuances around how you precisely define current total addressable market (TAM), management believes the $120 billion TAM figure is reasonable, meaning Stagwell has roughly 2% market share, so lots of blue sky to grow into.

Stagwell’s September 2022 Investor Presentation

As of Q2 FY 2022, Stagwell has over 13,000 employees, including over 1,300 software engineers. Stagwell’s TTM (twelve trailing month) revenue, as of June 30, 2022, was roughly $2.5 billion and its TTM Adj. EBITDA was $416 million.

As of August 4, 2022, and the mid-points, Stagwell has guided the street to FY 2022 20% organic net revenue, 15% organic net revenue growth ex-advocacy, $465 million of Adj. EBITDA, and approximately 30% free cash flow growth.

In addition, given the 2022 mid-term elections, Advocacy should have a very good second half 2022, notably in Q4 2022. Moreover, from a cash flow perspective, seasonally, Stagwell generates more free cash flow during the second half of the fiscal year.

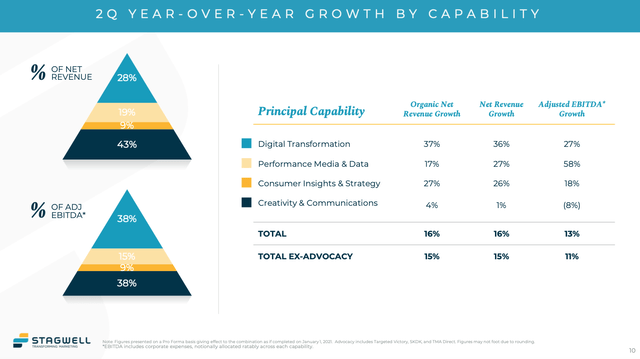

Stagwell is way out in front when it comes to digital and I really want to drive this point home as this what makes this investment compelling, at its current valuation. In Q2 FY 2022, the digital business experienced rapid organic revenue growth and very healthy Adj. EBITDA margins.

For perspective,

Our digital capabilities propelled our growth, increasing 28% organically on top of the last year’s 39% organic growth in the second quarter. Digital services contributed to 57% of net revenue and 62% of adjusted EBITDA in the quarter. Our unique mix of digital services is contributing to growth significantly higher than legacy companies in the industry, and will continue to propel us higher.

We’re growing our share of wallet with our largest clients. The average client size among the top 25 has grown from about $4.5 million to about $6 million, a 30% increase.

(Source: STGW’s Q2 FY 2022 Conference Call)

For additional context, enclosed below, see the slide below, which further details that digital growth.

Stagwell’s Q2 FY 2022 Earnings Presentation

(Source: Stagwell’s Q2 FY 2022 Investor Presentation)

Valuation And Peer Group

As Stagwell’s buyout/ merger with MDC Partners took place on August 2, 2021, therefore, I don’t have a clean full year set of numbers to make peer comparisons. So when you value this business, you really need to spread the numbers based on FY 2022 forecasts. However, for perspective, I did include Omnicom and Interpublic Group’s numbers to give readers some perspective and some peer comparison metrics. I intentionally excluded WPP plc, as they are London based, and the accounting and reporting in a 20-F are different than a 10-K, in the U.S. Given these differences, I didn’t want to risk an oversight as I’m just not well versed on International accounting standards.

Author’s Chart

As of its September 9, 2022 closing stock price, $7.15, STGW is trading at about 7.91X EV/ FY 2022 Adj. EBITDA guidance (at the mid-point). Now the big three generate a lot of operating cash flow and that cash flow can be used to pay a dividend, buyback shares, invest in the business, or pay down debt. Given the different point in their lifecycles, of the Big 3, compared to Stagwell, it is hard to make an apples to apples comparison.

That said, the reason for investing in Stagwell is to play the secular growth of integrated and digital marketing. Moreover, Stagwell’s organic revenue growth, driven by its strong arsenal of digital marketing brands, is growing at a much fast clip, in FY 2022 and beyond. In fact, back in November 2021, Mark originally guided the street to a long-term organic growth target of 7% to 9%, and in 2022, he upgraded that long-term organic annual revenue growth trajectory to 10% to 12%.

Why The Opportunity Exists

In this section, I will briefly theorize why this stock is trading a reasonable valuation given its really strong current and future growth rates.

1) The company came public via a buyout/ reverse merger. And just to be clear, this wasn’t a SPAC. Given this unconventional method of accessing the public market, there was no splashy IPO and therefore no fat underwriting fees for Wall Street. Sell side research has been on the decline for a long time, as it is a loss leader, in direct P/L terms. Therefore, Wall Street has fewer incentives to initiate coverage and sponsor a stock where there was no direct underwriting relationship. As a result, the vast majority of public equity investors don’t even know this company exists.

2) The company has only operated as a combined entity for just north of one year (since August 2, 2021). Therefore, the market has a much shorter operating history and it is harder to spread STGW’s numbers against its peer group and come up with a reasonable relatively value matrix.

3) If you read the Big 3’s 2022 as well as Stagwell’s 2022 earnings conference calls, you will quickly work out that the sell side is super concerned about the macro backdrop and what that means for 2023 organic growth rates (think slowing ad spending and businesses pull back on marketing to offset other inflationary spending pressures).

Incidentally, me and Mark spoke about this topic at lengthy. He said if you look at Google (GOOGL) you aren’t really seeing much of a slow down, but if you look at Meta Platforms, Inc. (META) you might draw a more pessimistic conclusion. However, if you take a step back, the slowdown at META is really driven by Apple privacy changes and increased competition from TikTok. Moreover, the divergence at a The Trade Desk, Inc. (TTD), so think strength, and weakness, at Roku, Inc. (ROKU), paint a more nuanced picture. Secondly, if you take a step back, Stagwell has 2% market share and its digital growth is robust, so the big marketers are still spending, as turning the marketing spigot off and on isn’t a sound long-term growth strategy for brands.

Lastly, as Mark stated on the Q2 FY 2022 conference call, it is no longer only a two horse race, where you have two choices – run on the digital rails of Facebook or Google – to reach your audience.

We believe many of the prevailing industry trends that are competitive headwinds for some of the dominant advertising platforms can be opportunities for Stagwell. The rise of new platforms and channels like TikTok, Connected TV, e-commerce marketplaces and digital out-of-home, increases the complexity of digital media buying and so more clients are turning to our state-of-the-art media buying operations in these emerging areas.

Risks

The biggest risk is execution risk. Stagwell has been highly acquisitive and made what appears to be a lot of smart acquisitions, not overpaying for good assets. However, there is an art to business integration and pursuing such rapid growth does inherently involve risks. Given all of the M&A, and we are talking relatively smaller dollars (think $25 million to $50 million type of deals as well as some bolt-on deals), but there is the risk that management has too many balls in the air and the organization gets too complex to fly, even for someone as capable as Captain James Tiberius Kirk.

Secondly, no question the macro is a concern, as the organic 2023 growth outlook is uncertain, for the broader advertising industry. 2021 was a great year for organic growth and the first half of 2022 has been solid. This uncertainty, whether justified or not, could act as gravity, and lead to moderate industry wide multiple compression.

Putting It All Together

A friend of mine worked for John Paulson, in 2009 and 2010, so just after Paulson & Co. was briefly the toast of Wall Street and assets were approaching $50 billion. Being at the right shop, at the right time, meant meeting with countless management teams and an upfront look at many different businesses. When he and I talk stocks, our perception of the management team always come up, and we have a phrase, ‘Is the team at company XYZ real?’. I would argue that Mark Penn and Stagwell Inc. are real.

Stagwell is the up and coming digital market company, arguably way out in front, at least on the digital front. This company has cleverly fused creative and technology to offer integrated marketing solutions and can run with the thoroughbreds, and on any racetrack.

In closing, I would argue investors have the chance to buy a good business, at a reasonable valuation (EV/ Adj. EBITDA). Stagwell is well positioned to win market share given its strong collection of brands and arguably the best vehicle to play digital marketing growth.